DISCLAIMER: Below is an article with ideas or a personal stance about finances. This article is not financial advice. Investing is risky. Please consult with a financial advisor before investing.

This article is part of a trilogy containing everything you need to get started with your own business, manage your portfolio, and amass generational wealth:

Part 1: Deciding What Type of Online Business to Start: 4 Deciding Factors

Part 2: Portfolio Management for Online Lifestyle Entrepreneurs: the 10triple30 portfolio

Part 3: 5 Layers of Wealth

When it comes to portfolio management, there’s an abundance of options out there: the classic 60/40 portfolio, mutual funds, 401k’s, index ETF’s like SPY, VOO, QQQ, IWM.

They all have one thing in common, they’re targetted towards people with a 9 to 5 job. Which makes sense since they are the large majority of people, but it leaves entrepreneurs having to fend for themselves. Why nobody is stopping you from picking one of the options above you will soon learn that, for an (online) entrepreneur, they’re suboptimal at best since they lack the flexibility you need.

[humix url=”https://www.bizfinlife.com/humix/video/MsF65PZzysf” float=”1″ autoplay=”1″ loop=”1″]

Why not go for a split that finds the Goldilock zone between flexibility and ROI?

As Robert Kiyosaki thought us, the rich don’t work for money, they work for assets. And those assets give us, as Grant Cardone taught us cashflow baby! To top it all off we’ll add a third quote that personally stuck with me from George Gammon: Any asset that doesn’t produce cashflow, is a speculation.

We’ve let these three wise men inspire us to come up with a portfolio that:

- Holds assets (duh)

- Provides us with cashflow (passive money, baby)

- Takes minimal management (we’re entrepreneurs first)

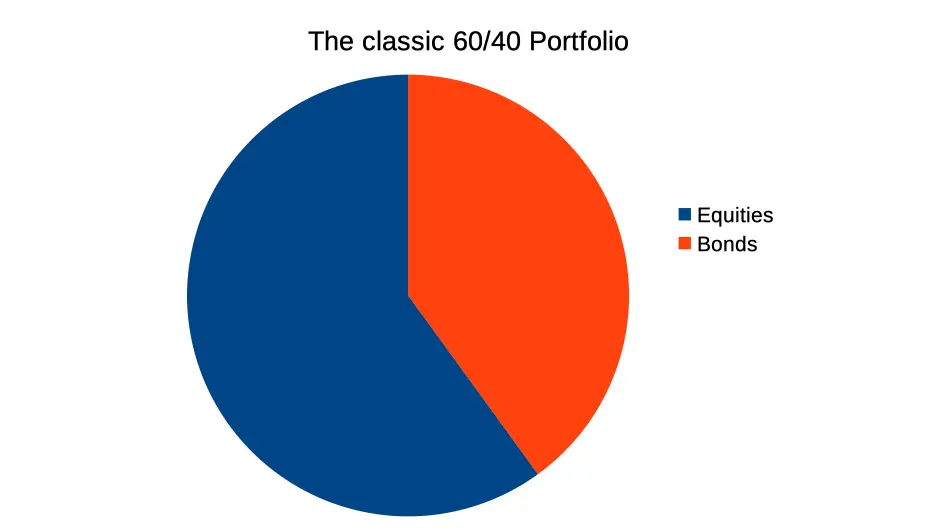

Doing it wrong: The 60/40 portfolio

For decades, the 60/40 portfolio was praised for its alleged safety and in an environment of decreasing interest rate, that mostly was the case.

The idea behind the 60/40 was that the 40% bond allocation would compensate for stocks in a downturn, limiting the downside during corrections or, dare we say the c-word, market crashes.

But the times, they are a-changin’ and with the intrest rate practically at zero there are no guarantees that in the future bonds will act as a hedge like they did in the past 40 years, making the 60/40 portfolio no longer the safe play it once was.

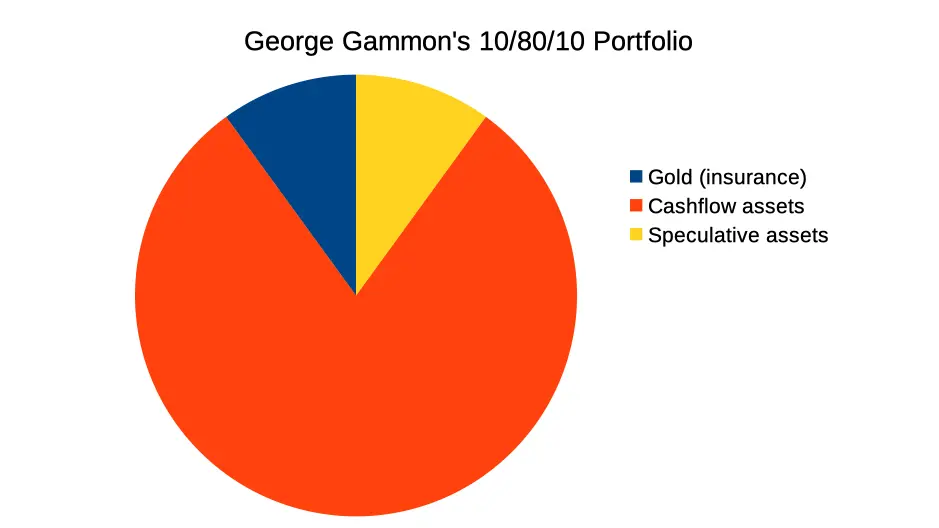

Doing it mostly right: The 10/80/10 portfolio

We’ve quoted George Gammon before, we’ll drag him in one more time to analyze his proposed portfolio: the 10/80/10 portfolio.

As an entrepreneur/investor, Gammon saw what was happing to intrest rates and warned agains the 60/40 portfolio, propose an entrepreneur-friendly alternative: a portfolio consisting of 10% gold as insurance, a big chunk of 80% of cashflow generating assets and another 10% for speculative assets.

As an entrepreneur you don’t need lines to color in so he left the 80% open for interpretation. This could be your own business, real estate, dividend stocks, technically you could even argue staked crypto falls in this category, although we feel that probably wasn’t Gammon’s intention.

As a general entrepreneur portfolio, we like this take, despite not being perfect there are some good ideas to start with, so in the next step we specify further to turn this general entrepreneur portfolio into a online lifestyle entrepreneur portfolio.

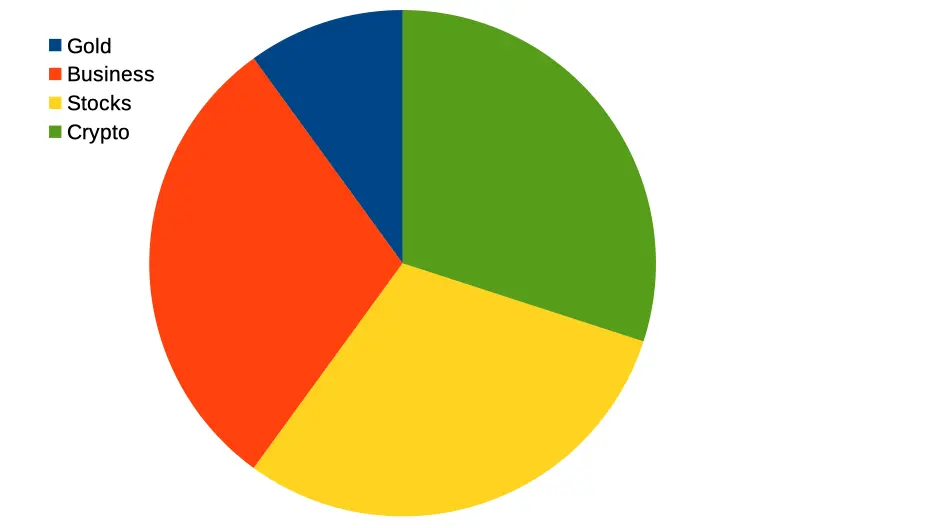

Perfection: The 10triple30 portfolio

We like cashflow, but we also like growth, especially if we have the time to wait. So we wanted to make the 10triple30 portfolio cashflow/growth agnostic. It’s really up to you if you want to aim for any of the two or take a more hybrid approach.

We wanted to have this portfolio be a baseline to get started with, like George Gammon did with his lare 80% block. We feel there’s no one-size-fits-all in this. If you want an easy solution, outsource it.

Metals: 10%

We like Gammon’s idea of insurance. Gold has proven to be that for 1000s of years. So did silver, which is also heavily used in industry, which is a nice bonus. So we’ve renamed the category to metals (know, we don’t throw Bitcoin in there as digital gold). Gold vs silver allocation we leave up to you.

Business: 30%

If you own a brick-and-mortar business it should probably be 80% of your net worth but since we’re lifestyle entrepreneurs and have no desire to become billionaires we aim for our active business to be about 30% of total net worth.

Stocks: 30%

As lifestyle entrepreneurs we also want to make some passive-ish money so we allocate another 30% to stocks. Whether you go for growth or cashflow again is up to you. There’s good cases to be made for both, the more stock cashflow the less you need to be dependend on your business and the more growth to quicker you can retire (but who really wants to retire from this lifestyle?)

Crypto: 30%

The final leg of the three-legged stool is designated to crypto. We’re young(-ish), we’re online, so why not have some internet-native currencies? Crypto is traditionally considered to be more speculative so one might argue we triple the speculation from the 10/80/10 portfolio, although, as we alluded earlier, there’s ways to make crypto cashflow trough staking or lending for example. Or you could use some of your crypto to invest in a cashflowing NFT.

Conclusion

There’s a reason we’re being deliberately vague. Everyone has different risk-tolerance, everyone is on a different stage in their life so you can make any category as cashflow/growth oriented as you want or conservative/speculative as you want. You can get 30% in altcoins and the other 30% in tech growth stocks or you can just as easily get 30% Bitcoin and 30% blue-chip dividend stocks. Add salt to taste…

Is the 10triple30 portfolio also 10/80/10?

While we went into further specifying categories, your 10triple30 portfolio can actually be a 10/80/10 portfolio at the same time. You could allocate your 10% metals entirely to gold, own 10% speculative alts and invest the rest in your own business, dividend stocks & safe stakes crypto. As we said, our main goal was for you to have a blueprint to start with but still retain as many options as possible.