DISCLAIMER: Below is an article with ideas or a personal stance about finances. This article is not financial advice. Investing is risky. Please consult with a financial advisor before investing.

This article is part of a trilogy containing everything you need to get started with your own business, manage your portfolio, and amass generational wealth:

Part 1: Deciding What Type of Online Business to Start: 4 Deciding Factors

Part 2: Portfolio Management for Online Lifestyle Entrepreneurs: the 10triple30 portfolio

Part 3: 5 Layers of Wealth

There’s an order to life. We’ve written about what business to start and how to manage your portfolio, now it’s time to look into using what we’ve learned from those two articles to amass real generational wealth.

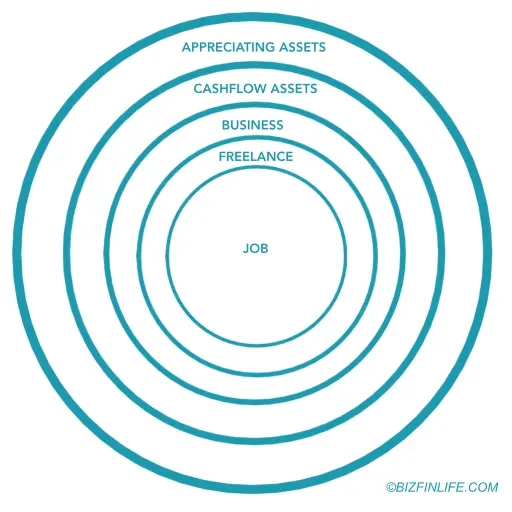

We’ve identified five layers, like an onion (or an ogre), you need to go through but you can easily look at them as five levels in a computer game or a flywheel speeding up as you travel through time.

The 5 layers of wealth is a proven strategy used by many great entrepreneurs and investors in the past to create generational wealth. It’s not a get-rich-overnight scheme. Completing this strategy in full will at the very least take many years, most likely decades. This is a long-term strategy.

[humix url=”https://www.bizfinlife.com/humix/video/p7EsyjZ45cf” float=”1″ autoplay=”1″ loop=”1″]

Before we look into the five layers, let’s quickly go over how to not get to the finish line.

Wrong Ways

Government Pension

Daddy government will take care of us, right? He promised!

Well, Daddy government is flat broke, spending money he doesn’t have and soon his lenders might come and collect.

Trusting on third parties to look after you is the worst way to go through this and might end in disappointment.

It’s much better to look at government pensions as a nice cherry on top but doesn’t expect them to bring you the pie.

401K

So I’ll just take care of myself by getting a 401K then. My employer might even match and on top of that, it’s tax-free!

First of all, they’re not tax-free, you just get taxed on the way out and if your portfolio performed well you might actually punish yourself because you’ll get taxed on your profits.

Roth IRA then? It pushes your tax burden to the front of the line but still doesn’t fix your other problems. High fees and limited investment options.

DCA into Index Funds

Well, then I’ll just manage my own portfolio. I’ll get some index funds to keep the fees to a minimum and just DCA into them. Compound interest, amirite?

Sure, you might skip the worst expenses but you still haven’t addressed the biggest problem, you’ve just changed your third-party dependency from the government to Wall Street, still giving you practically no control over your investment. You might be able to pick the funds, but you have no control over their performance.

The Elephant in the Room

These options lack many things but there’s one main problem they all have in common: the lack of control.

To be in charge of your own life and wealth you need to travel through the five layers of wealth in the exact order we’ve listed them below.

Layer One: Job

Also called Just Over Broke.

Limited Cashflow

We all start from layer one. An honest day’s pay for an honest day’s work. This is where 95% of people start and end never getting to even layer two. Some try but lack persistence, the majority never even bother to try.

Layer one will try to keep you in the “safe” middle trying to trap you with pensions, 401K’s, and health benefits but if you really want control over your life you need to escape it.

As Robert Kiyosaki said: “Work to learn, not to earn”. Use your job to gain experience and live below your means for a while until you have saved a proper safety cushion. Don’t bother with the stock market now, there’s no point in locking in gains this early down the race. Your money will be much more effective in the following layers.

Layer Two: Freelance

Active Cashflow

Once you’ve escaped the middle you’ll quickly start gaining some traction. Now you can use the experience acquired in layer one to sell your services to different customers. Diversifying your income is a good base to have before jumping onto the next layers.

Use your skills and network to raise your income further above your living expenses (don’t raise your living standard quite yet) and use your additional income to get started with your business.

Layer Three: Business

Semi-passive Cashflow

You still have your experience and customers from layers one and two, now is the time to properly get started in your business. Leverage up by either hiring people (employees or other freelancers) or using technology. Productive services or start creating digital or physical products to sell to your clientele.

Now the flywheel really starts spinning. Reinvest profits until you’re at a happy cash flow level, then look into jumping onto layer four. Keep your expenses low, you’re almost there!

Layer Four: Cashflow Assets

Passive Cashflow

When your business is producing enough cashflow you can look into gathering cashflowing assets.

Some good examples are rent, dividends, interest, and even a private business (run by a manager you hire) but also crypto (defi) and NFTs (virtual land) can be considered. It all depends on your boomerness.

Look into replacing your entire active income with passive income. It will give you options. Now you can take a more passive role in your business (outsourcing more) should you want to.

And at the end of layer four, you can wait for it, slightly even start increasing your lifestyle bit by bit (don’t worry, it’s optional. Keep living like a monk if you want).

Once your passive cash flow is higher than your living expenses it’s time to make the final jump onto layer five!

Layer Five: Appreciating Assets

Assets Appreciating in Value

Level five! Congratulations! You’ve made it onto the fifth and last layer for the final boss fight!

You now have enough cash flow from layer four for anything your heart desires (if it can be bought, at least), it’s now time to amass generational wealth.

Layer five is not that different from the previous layer except, since you no longer require your assets to produce cash flow, you can look into gathering assets that appreciate in value rather than produce cash flow, yielding often higher returns and not creating taxable events until you sell them.

A lot of these assets are similar to layer 4 like stocks, crypto, NFTs, or even real estate or a private business (or a combination of both) when set up right but this layer also unlocks new options like contemporary art, land or collectibles like classic cars.

Practical Action Plan

- Work your layer one job until you have a 6-12 month cushion and enough experience to go to the next layer

- Freelance for different clients and start a business on the side that doesn’t require you to trade time for money

- Work in your business and keep reinvesting profits until you no longer need to do freelancing.

- Convert additional business income into cash-flowing assets until passive income exceeds active income. Now you can quit the business or take a more passive approach allowing you to work on the business instead of in it.

- When passive cashflow is high enough to cover all your life expenses look into getting appreciating assets to hold over the long term. You are now generating generational wealth.

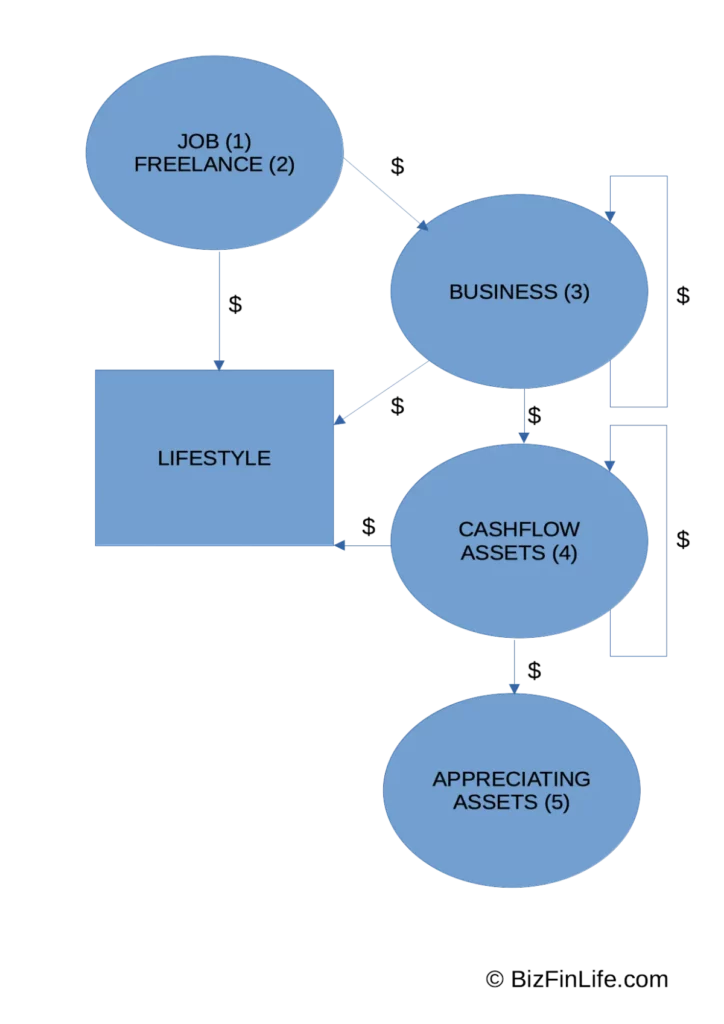

Or, since a picture says more than a thousand words…

The flowchart above points to where your income should stream, in the early years you’ll only make a little more than what’s necessary to fund your lifestyle, freelancing will increase this.

Then you can move some of the income to your business. There you can create a feedback loop by reinvesting everything you don’t need into your business. Later on, you can do the same with passive cashflow assets in the fourth layer.

When you jump from one layer to the next you can also gradually increase your lifestyle expenses. Keep in mind that the quicker you increase them, the longer it takes for the flywheel to speed up.

Eventually, in the last layer, you can hold assets that will just appreciate, there’s no need to feed them back since you’ll have enough cashflow already and there’s not really a need to sell anything (doing so will be a taxable event anyway so better to be avoided if not needed). Of course, there’s abilities to rotate expensive assets into cheaper ones along the way.